Economic paths diverged in Q1 as Covid-19 infections rose in many parts of the world once

more, leading to further restrictions. At the same time, the US and the UK accelerated their

vaccination programmes, allowing both countries to set a path to reopening well ahead of the

summer. Europe is now seeing an improved rollout as well, while Japan continues to lag. The

situation remains dire in many emerging economies, however, where the lengthy battle to slow

the spread of the virus continues to rage.

The US benefited from President Biden’s $1.9 trillion fiscal package, delivered promptly in a bid

to fuel growth and employment after a loss of momentum in late 2020. While other developed

countries have not seen anything like the same scale of fiscal support as the US, their

economies have nevertheless adapted to the stop-start nature the pandemic has brought and

have fared better than expected during recent bouts of restricted mobility

The US: peak in growth momentum in sight

More than a year has passed since Covid-19 hit the US, stopping the economy in its tracks.

Rapid monetary and fiscal support arrested the slide, lifted financial markets and left households

with additional liquidity even as unemployment rose. After a brief loss of momentum in the final

quarter of 2020, fiscal largesse set a course for the economy to recapture pre-Covid dollar levels

before the summer.

Biden’s first support package, totalling $1.9 trillion, was set in motion via reconciliation after a

swift rejection from the Republican Party. Further sizeable, longer-term programmes tackling

infrastructure, the environment and inequality, among other issues, will be harder to pass.

However, for now, the easing of restrictions for service providers together with bloated

household savings will drive growth of around 6% for this year and reinvigorate the employment

recovery over the coming months, even as less vaccinated states deal with the Delta variant.

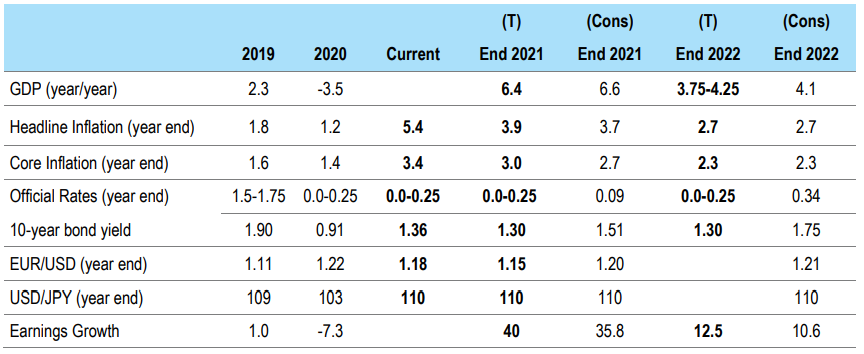

Figure 1: US forecasts

Source: Threadneedle Asset Management Limited/Bloomberg, August 2021. Notes: (T) = TAML forecast, (Cons) = consensus forecast *

denotes interim change. Changes to Threadneedle forecasts: GDP 2021 6.4 from 5.0; Headline Inflation 2021 2.3 from 2.0; Core Inflation

2021 2.2 from 1.7; EUR/USD 2021 1.15 from 1.27; USD/JPY 2021 110 from 100.

Continued support for the economy remains crucial. The Federal Reserve is acutely aware that

the pandemic has disproportionately hit low-income, minority households. Although the ongoing

quantitative easing program will likely be tapered in the new year, Fed Chairman Powell has

stated his intention to leave rates low for however long it takes to aid the repair.

Euro area: playing catch-up

After a stuttering start, Europe’s vaccination rollout has surpassed that of the US. The Delta

variant had a negative effect on Q2 GDP, but economies appear more resilient to restrictions

reintroduced in a number of countries

Indeed, indicators of economic sentiment remain on an upward trajectory, especially in

manufacturing where new orders appear to be driving a post-pandemic boom. So far, the “hard”

data does not reflect increased optimism; it is possible that lags are in play, that disrupted supply

chains are holding back production, or that surveys display excessive optimism, as they did

during the 2017 expansion.

The underlying health of the labour market may not be obvious for some time, as data here

continues to be distorted by large numbers of people engaged in short-term work programmes.

For now, optimism around a vigorous economic recovery rests with the consumer and a robust

run-down of the savings amassed over the past year or so. The largest share of foregone

consumption has occurred within services, where there are obvious limits as to how much can

be recouped. Additionally, as elsewhere, savings have tended to accumulate at the higher end

of both the income and demographic distributions where the propensity to consume is lower, all

else being equal.

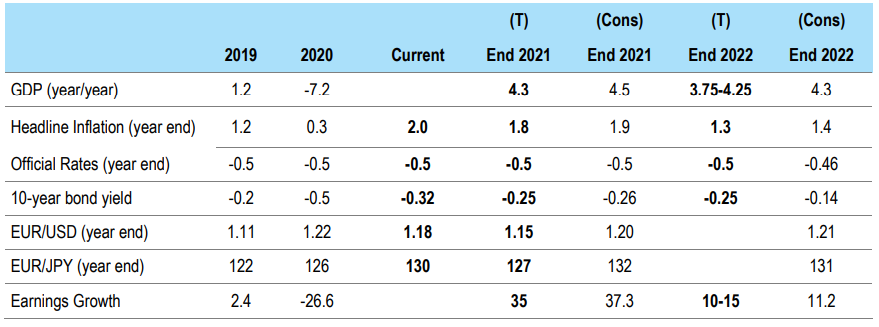

Figure 2: Euro area forecasts

Source: Threadneedle Asset Management Limited/Bloomberg, August 2021. Notes: (T) = TAML forecast, (Cons) = consensus forecast *

denotes interim change. Changes to Threadneedle forecasts: GDP 2021 4.3 from 4.0; Headline Inflation 2021 1.5 from 1.0; Official Rates

2021 -0.5 from -0.6; EUR/USD 2021 1.15 from 1.27.

The European fiscal response appears small compared with the combined US stimulus. In

contrast with their North American counterparts, household disposable incomes have stagnated

since the end of 2019 in the euro area, where support has been largely delivered via job

retention programmes. We believe this will likely lead to a less impressive recovery.

The European Central Bank has adjusted its policy framework closer to that of the Fed, in

allowing for an overshoot of inflation expectations over its forecast period. This implies a lengthy

extension to the existing easy policy. But medium-term hopes for a higher rate of GDP growth

are best pinned on an eventual rotation away from pro-cyclicality in member states’ budget

policies, as embodied in the eurozone’s fiscal framework. It seems likely that the EU’s Stability

and Growth Pact deficit and debt ratio requirements will be suspended until at least 2023.

Negotiations around more permanent changes are likely to resume later this year.

UK: bouncing back, for now

The reopening of the UK economy has continued apace, helped by the success of the

vaccination program. GDP has continued to make swift gains as sectors have gone from

generating zero to low levels of output. However, faster-moving indicators of growth, such as the

employee turnover and card spending data from the Office of National Statistics, point to a

deceleration in consumption growth after the initial burst of spending. The stock of excess

savings held by consumers remains the biggest upside risk to consumption, but the survey data

and details around where these savings are held continue to suggest that destocking will be

modest.

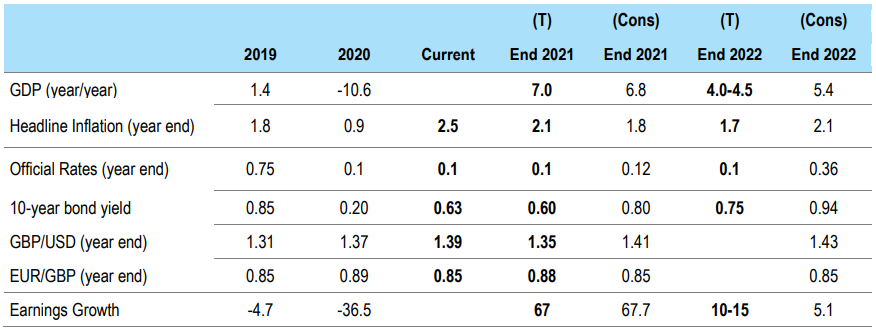

Figure 3: UK forecasts

Source: Threadneedle Asset Management Limited/Bloomberg, August 2021. Notes: (T) = TAML forecast, (Cons) = consensus forecast.

Changes to Threadneedle forecasts: GDP 2021 6.5 from 4.0; GDP 2022 4.5-5.0 from 5.5-6.0; Headline Inflation 2021 1.9 from 1.5; Official

Rates 2021 0.1 from -0.1; 10-Year Bond Yield 2021 0.75 from 0.25 GBP/USD 2021 1.30 from 1.40; EUR/GBP 2021 0.88 from 0.91.

Inflation is set to accelerate over coming months in line with global trends, as the inability of

supply chains to adjust to changing consumption patterns and Covid blockages in the near term

leads to higher prices. Wages also appear to be lifting sharply in certain industries such as

logistics and haulage, owing to labour shortages from the conflux of Brexit and Covid. A higher

clearing wage is likely required in the short term, but thereafter increased rates of wage growth

will not be necessary.

Against this backdrop of rising inflation in the near term, but still uncertain trends for growth and

inflation over the longer term, the Bank of England has become slightly more hawkish as the

year has progressed. The extent of policy tightening will be determined by the persistence of

above-trend levels of inflation, and we continue to believe that tightening will not need to be as

aggressive as the market is currently pricing in

Japan: another Covid wave delays a sustained consumer rebound

No changes have been made to Japanese forecasts: the 2021 GDP forecast remains at 3%.

This is above consensus and reliant on anticipated ongoing support from external demand,

unlike the contraction in 2020. Capex is also expected to pick up this year relative to 2020.

Until recently, Japan’s management of Covid had been one of the best in the world. However,

cases and deaths have spiked again, triggering the announcement of a fourth state of

emergency (SoE). This has prompted us to revise our projections on the start of the sustained

rebound in consumer spending to the end of Q3, when vaccine coverage should have picked up

significantly. Japan’s vaccination numbers are currently at around 40%, relative to around 60%

in other developed markets. However, the vaccination rate picked up relatively quickly once the

process started, suggesting that enough inoculations will have been administered by the end of

Q3 to avoid future SoEs

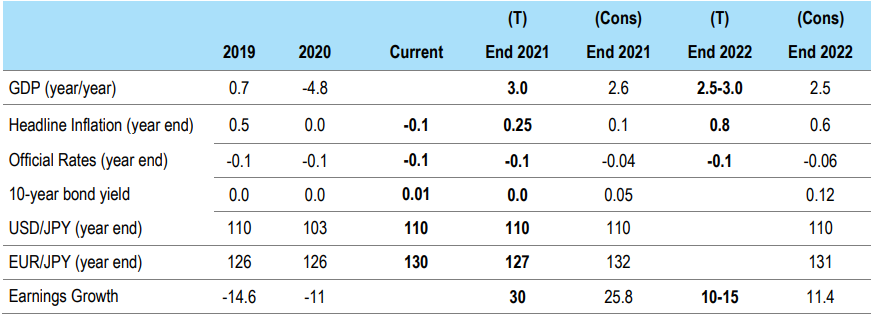

Figure 4: Japan forecasts

Source: Threadneedle Asset Management Limited/Bloomberg, August 2021. Notes: (T) = TAML forecast, (Cons) = consensus forecast.

Changes to Threadneedle forecasts: GDP 2021 3.5 from 4.0; Headline Inflation 2021 0.25 from 0.5; USD/JPY 2021 110 from 100.

The area of domestic demand that does look set for a strong year is corporate capex; realised

numbers tended to be higher than anticipated in early 2021 and the starting point this year is the

highest level in the past five years. On the external front, trade data remains encouraging and

points to further strong contributions to GDP from net exports in 2021. In addition, growth in

machine tool orders, which leads global and Japanese industrial production by around a quarter,

remain elevated.

Overall, we expect a continued slump in domestic activity until the end of Q3, but ongoing

support from the external component of the economy should make this less severe relative to

last year. Once vaccination levels pick up we expect a strong and sustained rebound in domestic

activity to coincide with ongoing strength in the external component of the economy.

China: balancing systemic risk management with unemployment

The Chinese government was quick to reduce systemic risk by deleveraging the local

government and property sectors. However, the broader environment has not been conducive to

lifting growth in the priority sectors, notably SMEs and manufacturing investments. The

government is also increasingly concerned over job creation. As such, we expect another cut to

the reserve requirement ratio (RRR) in Q4 in order to assure the banking system that liquidity will

not be prematurely or accidentally tightened. We also expect additional fiscal spending for new

infrastructure investments.

The impact on growth of deleveraging of the property sector is likely to be more negative than

the market currently expects. The growth in outstanding property developer bonds fell to -5.9%

year-on-year in Q2, from -2.7% in Q1 and 4.8% in Q4 2020 – well below pre-pandemic levels of

12.5% in 2019. The growth in outstanding RMB loans for property also fell to 9.5% in Q2 2021,

down from 10.9% in Q1 2021 and 14.8% in Q4 2020. This is important as the property sector

contributes between 12% and 16% of China’s GDP, and up to 44% of total tax revenue that

generally funds infrastructure investments at local levels. The growth impact of a contraction in

credit is generally felt with a lag of six to nine months. As such, a further slowdown is

forthcoming.

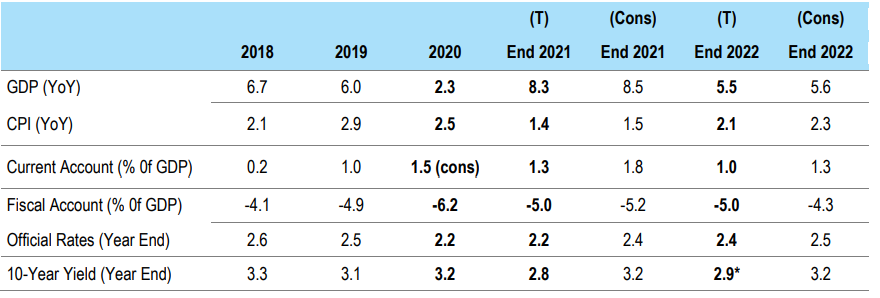

Figure 5: China forecasts

Source: Threadneedle Asset Management Limited/Bloomberg, August 2021. Notes: (T) = TAML forecast, (Cons) = consensus forecast.

This ultimately begs the question of whether China’s recent RRR cut is the start of another

easing cycle, and the extent to which there will be a potential loosening of restrictions and

regulations to prop up overall growth. The latter is unlikely given the recent announcement of

local government debt borrowing criteria and mortgage rate increases in Shanghai. Instead, the

government is expected to increase its efforts to reallocate credit towards manufacturing SMEs,

as these companies are experiencing a further slowdown in hiring and profit growth due to the

surge in raw material prices and shipping costs. For context, in China more than 98.7% of all

firms are small businesses with 300 or fewer employees, which contribute more than 60% to

total GDP and 75% to job creation figures. This segment is also crucial for domestic demand.

In summary, credit growth should stabilise at around 11% in the second half of 2021 from in

excess of 13% in December 2020. Increased government bond issuance and manufacturing

investments/loans to SMEs should offset lower property developer bond issuances and

household mortgages. Ultimately, the government’s aim is to avoid financial asset and debt

bubbles, reduce vulnerabilities to external policy factors, and increase domestic demand. So

long as the target surveyed urban unemployment rate of around 5.5% can be achieved, and 11

million jobs can be created this year, these structural reforms will continue.

Emerging markets: deceleration in the pace of growth

So far in 2021 there has been a divergence in the pace of growth between the US and the rest of

the world. Emerging market (EM) growth has been buoyed by export demand, specifically

commodity demand from the US and China. This driver is expected to normalise in the second

half of the year, with countries likely to depend more on domestic demand to sustain growth.

Looking at recent changes to growth outlooks, forecasts for growth in Asia have been marked

down more than 1% apart from in China and Japan. The main drivers are the resurgence in

Covid-19 cases and supply chain bottlenecks. On the other hand, stimulus has been supportive of

growth in Latin America and EMEA.

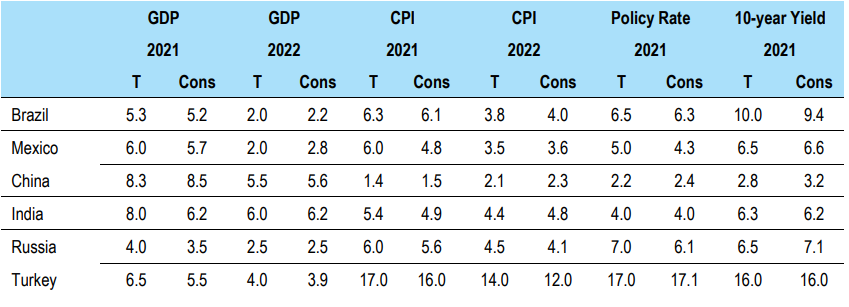

Figure 6: EM forecasts

Source: Threadneedle Asset Management Limited, Bloomberg, April 2021. Notes: (T) = TAML forecast, (Cons) = consensus forecast

Two downside risks to track include the resurgence of Covid due to lower vaccination rates in

EMs, and the ability of these countries to sustain incremental stimulus. Fiscal consolidation has

been pushed out, and countries with more vulnerable balance sheets are less able to continue

funding stimulus. Stimulus is largely funded via domestic markets and, in rare instances,

stabilisation funds. While foreign participation has been declining as a percentage of total funding,

debt financing costs have remained low and market access remains healthy

Regarding monetary policy in domestic markets, a broad tightening cycle is underway as EM

central banks front-run the Fed and respond to domestic inflationary pressures. Current account

balances have not been a material concern so far because domestic demand has been muted,

but we are expecting this trend to turn around in the next year as domestic demand returns.

The political environment in EMs reflects limited government support and rapidly rising poverty

rates, which could result in increased uncertainty around political transitions and social unrest.

Rising food prices are historically a precursor to instability in EMs, and this year is no different.

Corporate profitability recovered quickly in EMs. With lower vaccination rates there is continued

uncertainty around Covid. Therefore, we expect most EM corporates to continue to prioritise

deleveraging and capex in the second half of 2021, but increased pressure is likely to make

shareholder distributions a focus in 2022.

In summary, we expect continued growth at a slower pace in EMs.